Public Adjuster vs. Insurance Company Adjuster — What Austin Homeowners Must Understand

April 6, 2026 8:40 pmWhen your Austin home is damaged, one of the first steps in the claims process is an inspection.

Most homeowners assume the person evaluating their damage is there to help them.

That’s not always the case.

What many Austin homeowners don’t realize is that there are two different types of adjusters — and who they work for directly affects how much money you receive.

That’s where Mike Acerra comes in.

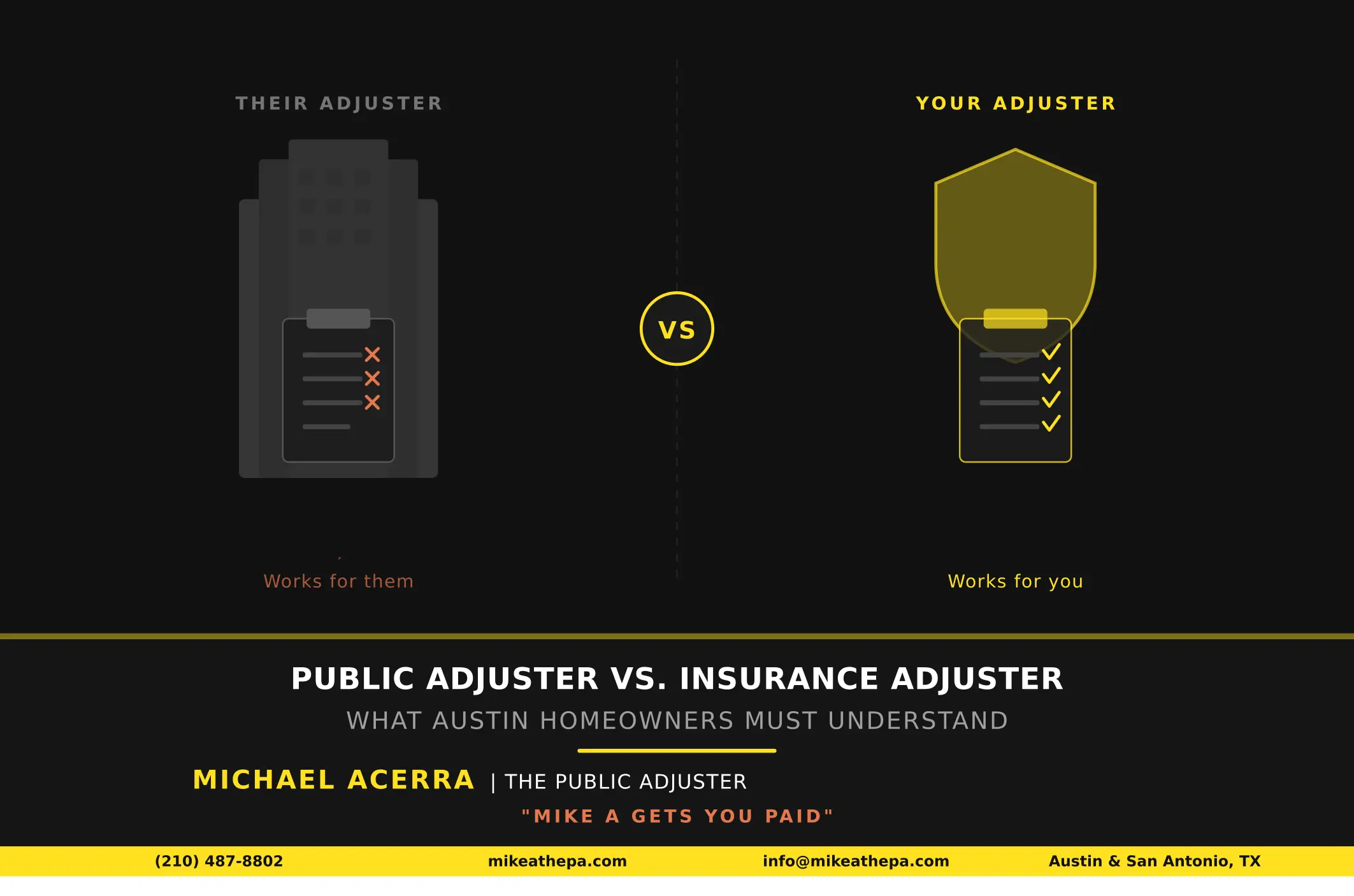

What Is the Difference Between an Insurance Adjuster and a Public Adjuster?

The difference is simple — but critical.

- An insurance adjuster works for the insurance company

- A public adjuster works for you

Both assess damage. Both prepare estimates. But their incentives — and outcomes — are very different.

Why Austin Homeowners Are at a Disadvantage

Austin’s storm environment creates a high-pressure claims system.

- Frequent hail storms generate massive claim volumes

- Insurance adjusters often handle large backlogs

- Inspections become quick and surface-level

This leads to:

- Missed damage

- Incomplete estimates

- Lower settlement offers

On top of that, many Austin homeowners are unfamiliar with:

- Texas-specific policy structures

- Wind and hail deductibles

- Coverage limitations for flood and water damage

This knowledge gap often results in underpaid claims.

What the Insurance Company’s Adjuster Does

When you file a claim, your insurer sends their adjuster — either a staff adjuster or an independent contractor.

Their role is to:

- Inspect your property

- Document damage

- Estimate repair costs

- Apply policy coverage

While many are professional, they ultimately represent the insurance company’s interests.

In practice, this can mean:

- Narrowing the scope of damage

- Missing less visible issues

- Producing estimates that favor lower payouts

What Mike Acerra Does for You as a Public Adjuster

When you hire Mike Acerra, you gain an advocate focused entirely on your outcome.

Here’s what you get:

- Thorough independent inspection

Identifies visible and hidden damage, including structural and system-level issues. - Complete documentation

Detailed reports and evidence aligned with policy language. - Policy review

Ensures all applicable coverages are identified and used. - Claim strategy and positioning

Builds a strong, well-supported claim before and during insurer review. - Direct negotiation

Handles all communication with the insurance company.

Unlike the insurance adjuster, Mike is financially motivated to maximize your claim, not minimize it.

Why This Matters Specifically in Austin

Austin damage scenarios are rarely simple.

- Hail damage can affect multiple roof layers beyond visible impact

- Flood and water damage can spread into walls, flooring, and structural systems

- Freeze damage can cascade across plumbing and interior finishes

These complexities are often missed in quick inspections.

Having a public adjuster ensures:

- Full scope identification

- Accurate documentation

- Stronger claim positioning

Common Questions — Answered

“My insurance company seems trustworthy. Do I still need a public adjuster?”

Yes. Even good insurers can underpay due to limited inspections or incomplete scope.

“Will this create conflict with my insurance company?”

No. Most claims are resolved professionally through documentation and negotiation.

“Should I hire a lawyer instead?”

Lawyers are for litigation. Public adjusters are specialists in claim evaluation and negotiation, which is what most cases require.

The Cost of Handling Your Claim Alone

Without proper representation, homeowners risk:

- Missed or overlooked damage

- Reduced claim payouts

- Settlements that don’t fully cover repairs

Public adjusters work on contingency:

- No upfront cost

- No fee unless your claim increases

Serving Austin and Surrounding Areas

Mike Acerra serves homeowners across:

- Austin

- Cedar Park

- Round Rock

- Pflugerville

- Georgetown

- Kyle

- Buda

He understands Austin’s storm patterns, Texas insurance policies, and how to properly present claims.

Get a Free Property Inspection

If your home has been damaged, you don’t have to rely solely on the insurance company’s evaluation.

Get an independent assessment first.

Contact Mike Acerra today for a free inspection and claim review.

There’s no upfront cost — and no fee unless more is recovered for you.

Categorised in: Insurance, Public Adjuster

This post was written by pollylorenzo.digital@gmail.com

Comments are closed here.